Growth, Delinquencies & the FinTech Dilemma

A deep dive into the latest TransUnion report reveals fast growth, rising risk, and shifting signs for digital lenders.

India’s FinTech revolution has rewritten the rules of credit access. With just a smartphone and a few clicks, millions now access loans in seconds—no bank visits, no paperwork, no legacy friction. But beneath this impressive growth story lies a deeper question: Are we building a resilient credit system or racing toward a risk cliff ?

The TransUnion CIBIL FinTech Compass Report (April 2025) offers the most comprehensive snapshot yet of India’s digital lending ecosystem. It celebrates FinTechs’ innovation and reach, but also flags emerging fault lines—rising delinquencies, behavioral risk patterns, and signs of overexposure in key borrower segments.

Here are 7 sharp insights from the report :

1. 📈 FinTechs Are Winning the Volume Game

But credit quality concerns are rising

FinTech lenders now account for 89% of all small-ticket personal loan (STPL) new accounts (count) and serve over 23 million live retail borrowers, growing 15% YoY.

This dominance showcases how digital-first lenders have made credit access seamless for urban millennials and underserved consumers. But as volume scales up, vintage delinquency curves show clear signs of stress—especially post the 3-month mark from origination.

Speedy originations without deeper underwriting are inflating risk

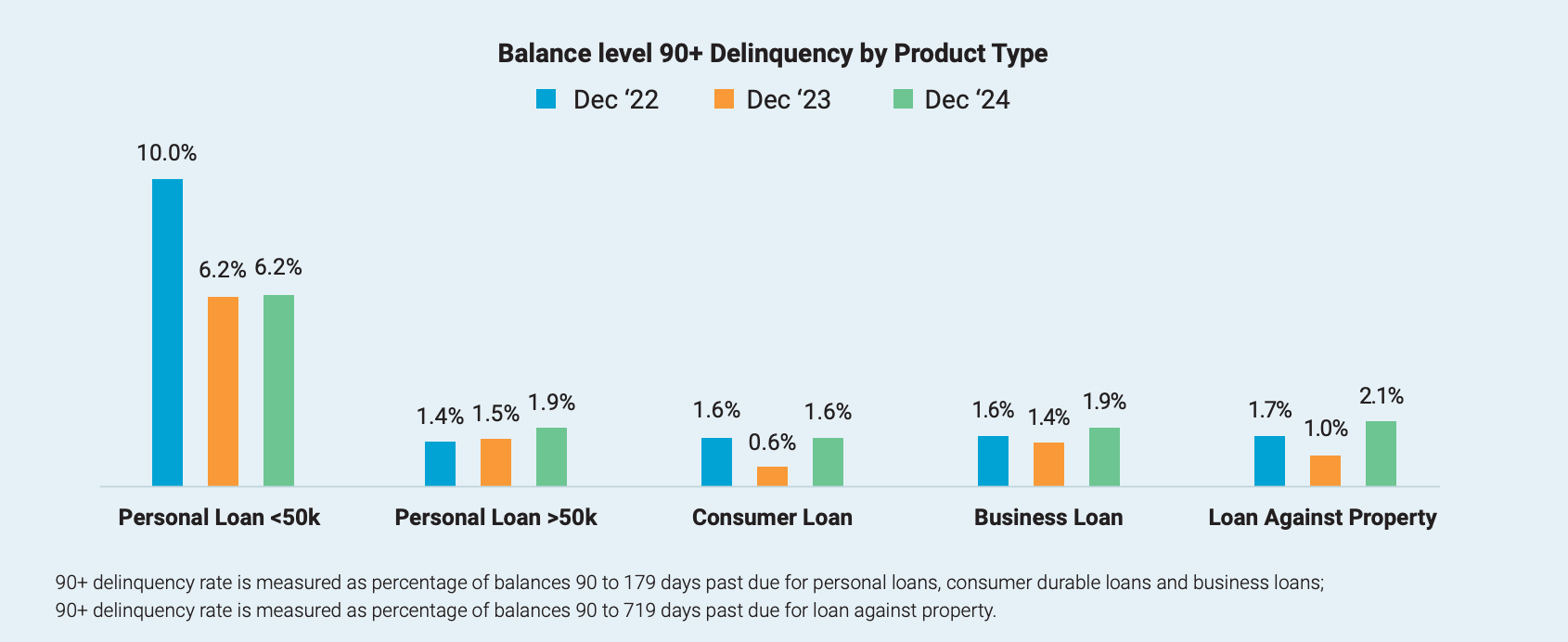

2. ⚠️ Delinquencies Are Creeping Up—Especially in Secured and Business Loans

90+ day delinquencies in business loans and LAP have increased YoY.

The increase in 90+ day delinquencies for Business loans and LAP suggests economic pressures on borrowers, possibly due to rising interest rates or sectoral slowdowns.

Roll-forward rates in early delinquency buckets (1–29 DPD and 30–59 DPD) are also high for STPL and consumer durable loans (>60%)—indicating that stress starts early in the cycle.

High roll-forward rates highlight the need for proactive collections. Early warning systems and personalized repayment plans can mitigate risks and improve recovery rates.

Collection strategies need to be reimagined for digital borrowers who default early and roll forward quickly.

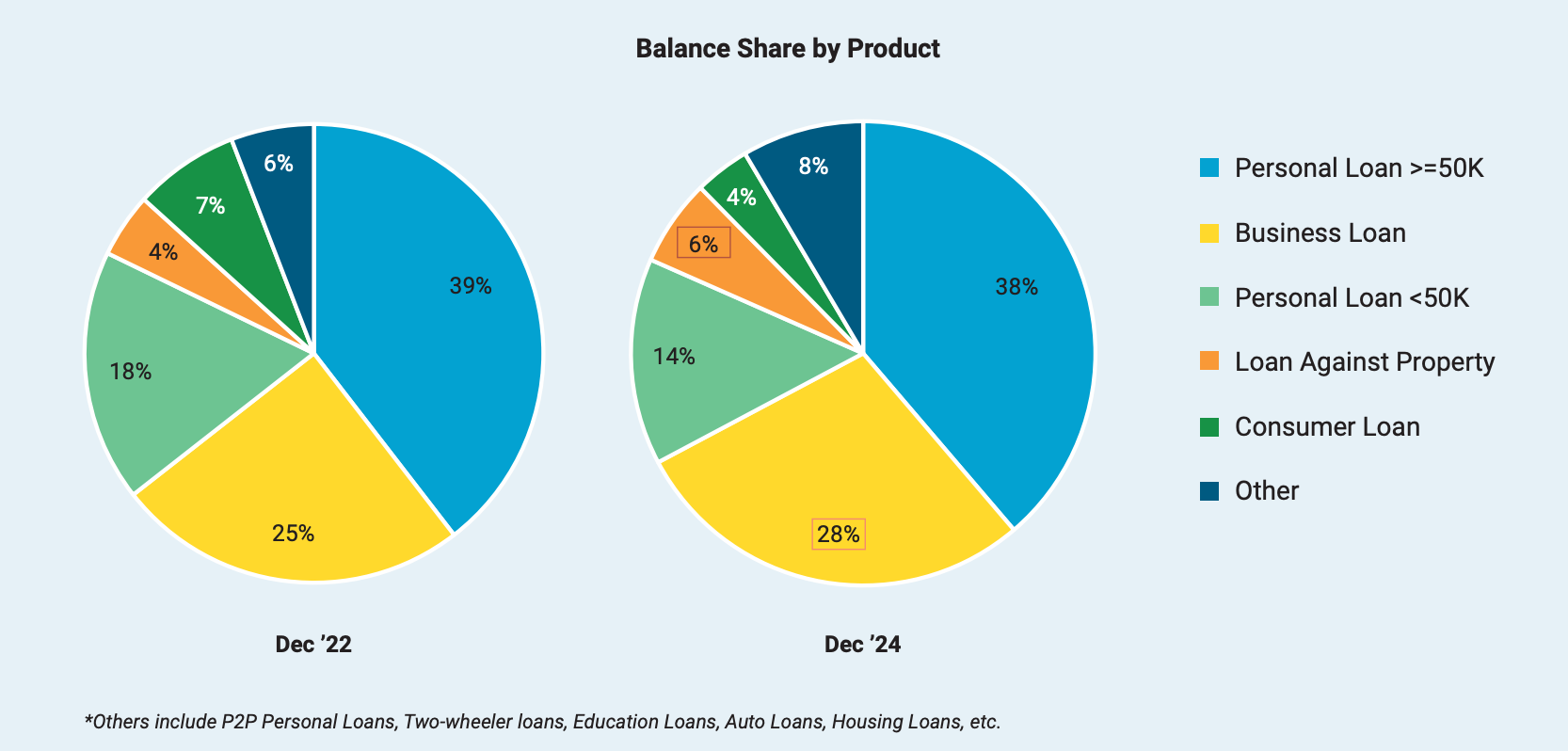

3. 🧲 Product Mix Is Evolving—But STPL Still Dominates

FinTechs have diversified into business loans, LAP, and consumer loans, but 92% of new accounts still are small-ticket personal loans (STPL).

The trend supports financial inclusion by catering to micro-entrepreneurs and rural consumers, key segments for economic growth. The report shows that from Dec 2022 to Dec 2024 explaining that the Fintechs are foraying into new products:

Share of business loans rose from 25% to 28%

Share of LAP increased from 4% to 6%

Yet, STPL continues to account for nearly all loan volume (by count)

Strengthening underwriting and customer retention will be key to long-term success.

Balance growth is coming from product breadth, but volume is still trapped in STPL.

4. 🌱 NTC Borrowers Form a Small But Strategic Share for FinTechs

Just 7% of FinTech personal loan borrowers are new-to-credit (NTC), compared to 9% for the rest of the industry.

Contrary to popular belief, FinTechs are not leading in onboarding NTCs. This may reflect post-pandemic risk aversion or a preference for low-friction, repeat borrowers.

The share of FinTech borrowers with a CreditVision (CV) score above 731 has risen sharply—from 47% in Dec 2022 to 59% in Dec 2024—indicating a clear shift toward lending to lower-risk, more creditworthy consumers. The shift toward prime consumers reduces credit risk, as these borrowers typically have lower default rates. However, FinTechs’ focus on existing credit consumers may limit their reach to new-to-credit (NTC) segments, a key driver of financial inclusion.

Yet, the NTC segment remains vital—especially in rural and semi-urban markets. Balancing risk and inclusion will be critical for sustained growth.

The next leap in financial inclusion will come from intelligent NTC underwriting—not just scale.

5. 🧮 Existing Borrowers Aren’t Always Safer

For personal loans >₹50,000, delinquency has risen slightly in “existing-to-lender” (ETL) borrowers.

Traditionally, repeat borrowers were considered low-risk. But FinTech data shows a 20 basis point increase in early delinquencies among ETL customers YoY. Although modest but warrants attention, as repeat customers are typically lower risk. What can help the fintechs to analyze comprehensive credit behaviors identify finer risk segments and tailored interventions ? (Next Segment)

This is the only segment where the delinquency has increased.

Even loyal customers need dynamic re-scoring and fresh affordability checks.

6. 🌀 Risk Rises With Borrower Over-Activity

The more loans a customer opens in a short time, the higher the early delinquency.

High inquiry rates and credit card utilization among borrowers indicate credit hunger, a common trend in India’s aspirational middle class. FinTechs’ ability to segment these behaviors can drive targeted product offerings, supporting economic growth.

The report reveals a sharp rise in 6-month 30+% rates based on:

number of loans opened in past 6 months

>6 loans = 9.7% , with 26% such population

Number of retail inquiries in past 12 months

>5 inquiries = 13.5%

This highlights a worrying behavioral trend—credit-hungry consumers stacking multiple loans in quick succession.

Examining recent disbursements with comprehensive credit behaviors can help in identifying finer risk segments. These tools can enhance risk differentiation, improve underwriting, and optimize debt management

FinTechs must flag behavioral risk early—based on multiple algorithms such as inquiries, open trades, and card utilization—not just scores.

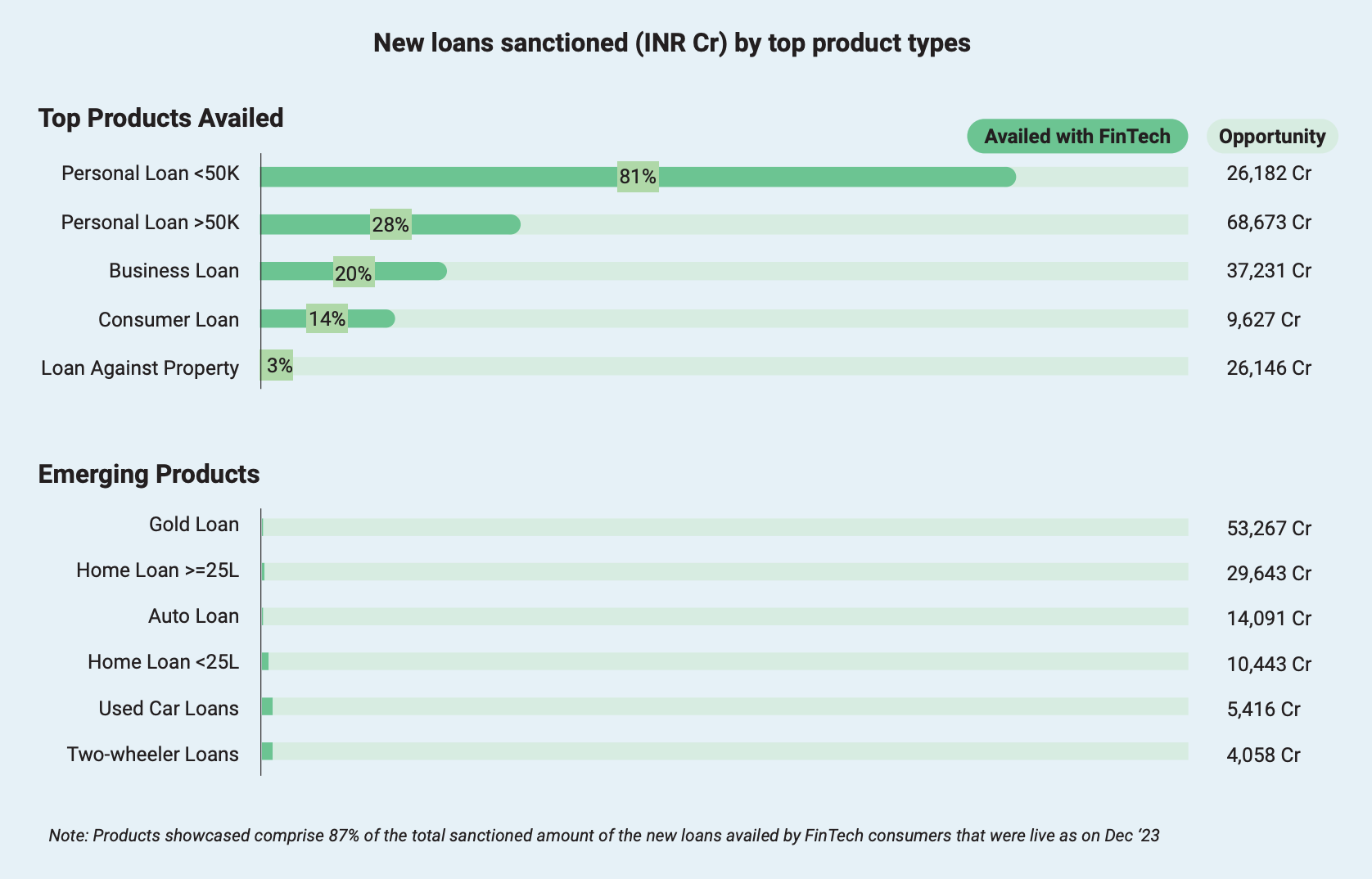

7. 🛣️ The Road to Diversification is Wide Open

FinTech users are already availing business loans, LAPs, and consumer durable loans—but from others.

From Jan–June 2024, overall consumers borrowed significant sanctioned amounts for business loans (~37k Cr) and loans against property (25k Cr) reflect strong consumer demand for secured financing, driven by India’s entrepreneurial and real estate sectors.

Emerging products like gold loans (~53k Cr) and home loans >25L (~30k Cr) suggest FinTechs can tap into aspirational consumer segments.

Yet only a small share of these were financed by FinTechs. This reveals a big opportunity.

FinTechs must move from STPL dominance to full-lifecycle financial partners.

Diversifying into secured products reduces reliance on unsecured STPL but introduces complexities in risk management, such as collateral valuation and legal compliance. The low customer loyalty for non-STPL products indicates FinTechs must improve product differentiation and customer experience to compete with traditional lenders.

Probable key to this shift:

Product innovation

Cross-sell engines with high customer engaagements

Risk-adjusted pricing for secured products

🧭 Final Thoughts: From Growth to Governance

The FinTech lending landscape is no longer in its experimental phase—it's mainstream, systemic, and deeply embedded in India’s credit backbone. With great reach comes great responsibility.

This TransUnion report is not just a retrospective—it’s a strategic risk guide. It reminds us that credit quality is not a tech problem—it’s a discipline problem. FinTechs must now evolve from acquisition machines to asset managers, from speed-led growth to precision-led sustainability.

The next big disruptor in lending won’t be faster apps or fancier UIs—it will be smarter risk intelligence, deeper borrower context, and real-time portfolio governance.

What do you think, do share your thoughts in the commets?

You can also download the report here.